What the FAQ are Security Tokens?

In this article we will be identifying the current landscape behind security tokens, defining what they are, understanding their purpose in the economy, and then completing a security token offering of our own to really make it all sink in.

The Surge of Crypto Capital

With World Blockchain Forum’s Securities Tokens and ICOs event coming down the pipeline, I've been receiving a lot of questions concerning security tokens. Most of these conversations are hinged on the differences between utility versus securities, and how the crypto capital explosion of Initial Coin Offerings (ICOs) will effect their investments as regulators start to figure out what’s going on under the hood.

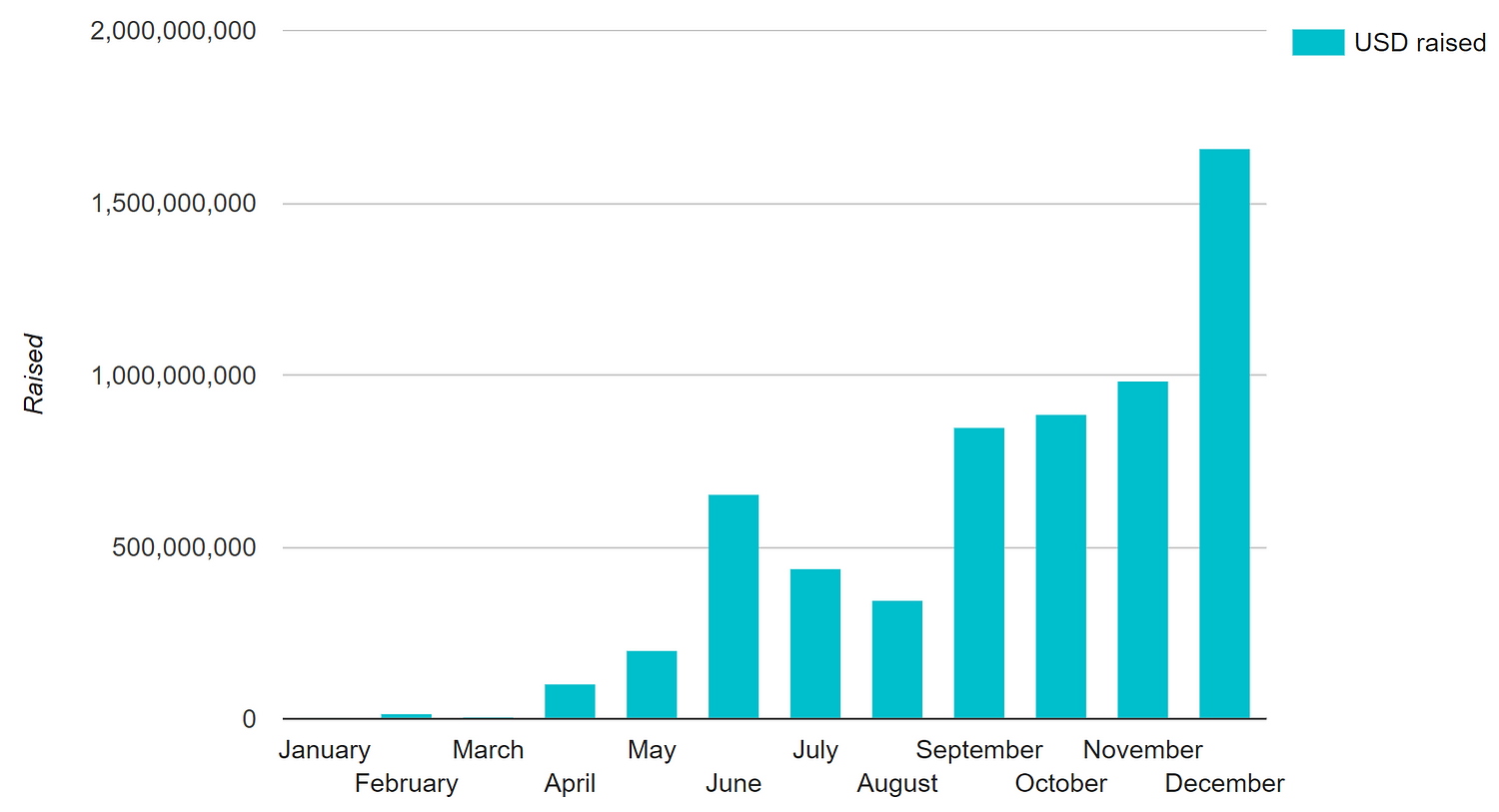

To put the capital raising taking place in the cryptocurrency markets into perspective, ICOs raised over $6 billion in 2017, and have since exceeded that figure in 2018 alone. For a market with very little working products, there sure is a lot of capital being poured into it!